In a world where digital-first experiences are now the norm, legacy loan origination systems (LOS) are under growing pressure to evolve—or risk falling behind. Despite increased demand for inclusive, efficient lending, many banks and NBFCs still grapple with fragmented systems, hard-coded workflows, and opaque decisioning processes.

According to IBS Intelligence’s Global Lending Report (2025), over 65% of global lenders cite “workflow rigidity” and “integration complexity” as the top two barriers to modernizing their LOS infrastructure. These constraints slow down disbursals, new product launches and inflate operational costs, thereby limiting the ability to serve new borrower segments.

The Cracks in the Conventional Model

Traditional LOS frameworks were built for a paper-driven world. Designed with hardcoded logic and fixed credit models, they struggle to adapt to the needs of modern lending:

- One-size-fits-all products: Most systems lack the flexibility to cater to diverse borrower types or loan products. Whether it’s a salaried individual or a rural MSME, the same approval workflow applies—leading to suboptimal customer experiences.

- High cost of origination: In the old model, all data—whether essential or not—was collected upfront. This meant lenders incurred full data retrieval and processing costs even if a borrower failed the first eligibility check.

- Opaque eligibility decisions: Borrowers were often left in the dark. A rejected application didn’t reveal whether it was due to a poor credit score, insufficient income, or documentation gaps.

As world turns digital-first, the lenders need to address these inefficiencies to remain competitive, delivering best in class customer experience and improving RoE. Rethinking LOS as a dynamic, data-driven layer of intelligence rather than a static back-office tool.

WonderLend Hubs: A Modular LOS for Modern Lending

WonderLend Hubs, a Cedar-IBSi Capital portfolio company is leading the charge. Their platform—built as a low-code, micro-modular PaaS—is designed to give lenders control over how they originate, underwrite, and disburse credit across diverse products.

Here are a few of their key differentiators:

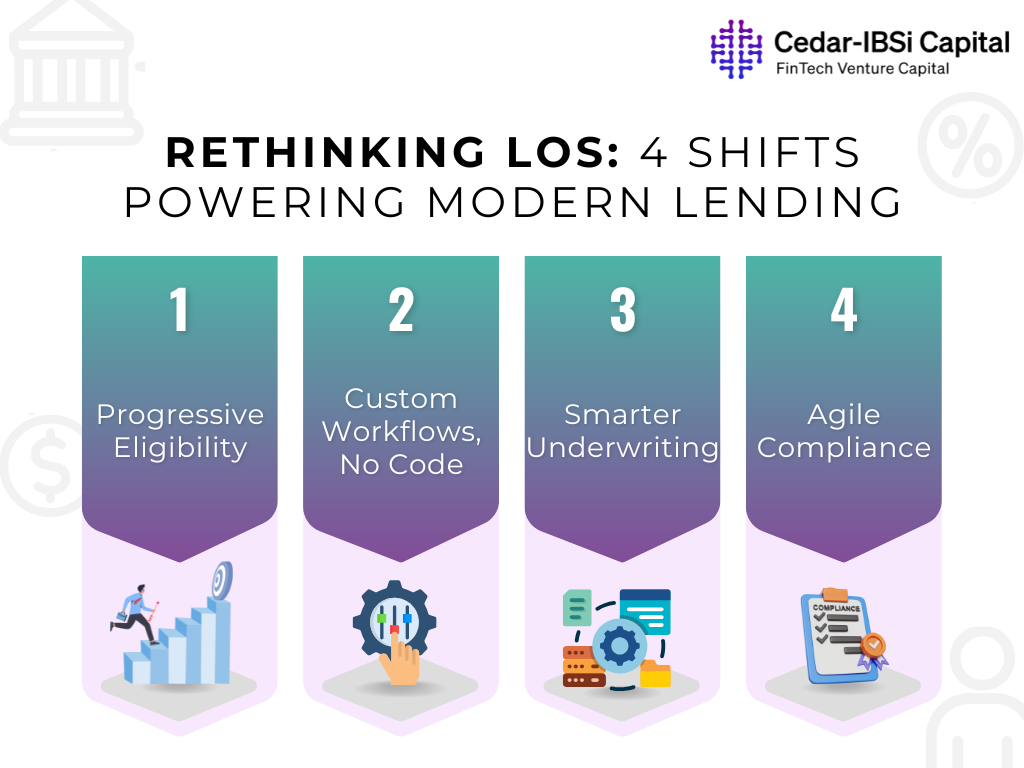

1. Multi-path Eligibility Decisioning

Unlike legacy systems that demand a complete borrower profile upfront, WonderLend allows eligibility to be assessed progressively—starting with minimal data such as a bank statement or GST filing.

This “stage-gated” approach helps lenders optimize cost-to-decision ratios while offering tailored loan options. A borrower might qualify for ₹1.5L based on GST filings, but ₹3L if they submit verified P&L data.

2. Custom Journeys Based on Product, Borrower Type, and Policy

WonderLend’s LOS lets business teams create and update lending workflows—without writing code. Whether the applicant is a salaried professional applying for a personal loan or a small business owner seeking working capital, workflows can differ not just by product, but by user type.

This agility helped one of their large NBFC clients—launch a digital MSME product, something they couldn’t do with their legacy system. The traditional system lacked the flexibility to ingest digital data and build configurable journeys aligned with new business models.

3. Contextual Use of Alternate Data

By tapping into digital sources like GST filings, UPI transactions, psychometric assessments, and real-time bank statements, WonderLend enables underwriting models that go beyond bureau scores. This opens up “thin file” borrower segments that were traditionally underserved.

As cited in IBSI’s report, leading platforms are already seeing 20–30% higher approval rates for MSMEs when alternate data is combined with traditional financials.

4. Compliance-Ready and Rapidly Adaptable

Regulatory changes (e.g., India’s new digital lending guidelines) often leave traditional LOS teams scrambling. WonderLend’s architecture, however, enables near real-time updates to policy rules and workflows. This not only improves time-to-compliance but gives lenders the agility to stay ahead of regulatory curveballs.

The Bigger Picture: LOS as a Strategic Growth Lever

Modern LOS platforms like WonderLend are now leaning more toward intelligence, adaptability, and customer-centricity. As the lending landscape becomes more fragmented and competitive, the ability to design unique credit journeys quickly and cost-effectively will define winners.

To quote WonderLend’s leadership:

“Lending used to be imprisoned by paper and processes. Today, we’re freeing it with flexibility and data.” If banks and NBFCs want to keep pace with evolving borrower expectations, their LOS must become the engine driving inclusive, scalable, and intelligent credit delivery.