We can no longer imagine a world without fast digital payments, yet as the volume surges, the backbone of the payment ecosystem—processing systems—is showing its age. These systems have powered global commerce for decades, yet their rigidity, complexity, and lack of transparency are increasingly becoming bottlenecks.

The Legacy Stack: Built for Yesterday

Traditional payment processing systems were designed in an era of batch processing, limited interoperability, and closed-loop networks. Today, they struggle with:

- Difficulty in scaling or modifying – Monolithic architecture;

- Prone to errors and delays – still requires manual reconciliation;

- Interchange, scheme fees, and MDR often lack transparency – Opaque fee structures;

- Fraud detection and dispute resolution – Limited real-time capabilities;

- Banks and merchants are tied to an outdated tech stack – leading to Vendor lock-in.

These systems are often maintained by large processors and banks, who prioritise stability over innovation. But in a fast-moving digital economy, stability without agility is a liability.

Where the Cracks Are Showing

- Routing Inefficiencies

Legacy systems lack intelligent routing based on cost, speed, or risk. Need smart switches that optimise transaction flows. - Clearing & Settlement Delays

While UPI and IMPS offer real-time payments, settlement cycles for cards and aggregators often follow T+1 or T+2 timelines. This affects merchant cash flows and financial planning. Real-time settlement is not just possible—it’s expected. - Reconciliation Nightmares

Enterprises face challenges reconciling transactions across multiple PSPs and revenue streams. Multiple data formats, fragmented systems, and manual processes make reconciliation a pain point. This leads to delays, mismatches, and operational overhead, which can be mitigated through possible automation with AI and APIs. - Risk Management Gaps

Rise in small-value transaction frauds and evolving fraud patterns leave many PSPs still relying on static rule engines vulnerable. RBI and FinTechs are pushing for AI/ML-based fraud detection, but adoption is uneven. - Dispute Resolution Bottlenecks

Chargebacks are slow and opaque, especially in card-based and cross-border transactions. Lack of standardised workflows across PSPs and banks. It needs transparent, trackable dispute workflows with customer-centric UX.

The Startup Opportunity

For startups, this isn’t a problem—it’s an opportunity where startups are capitalising.

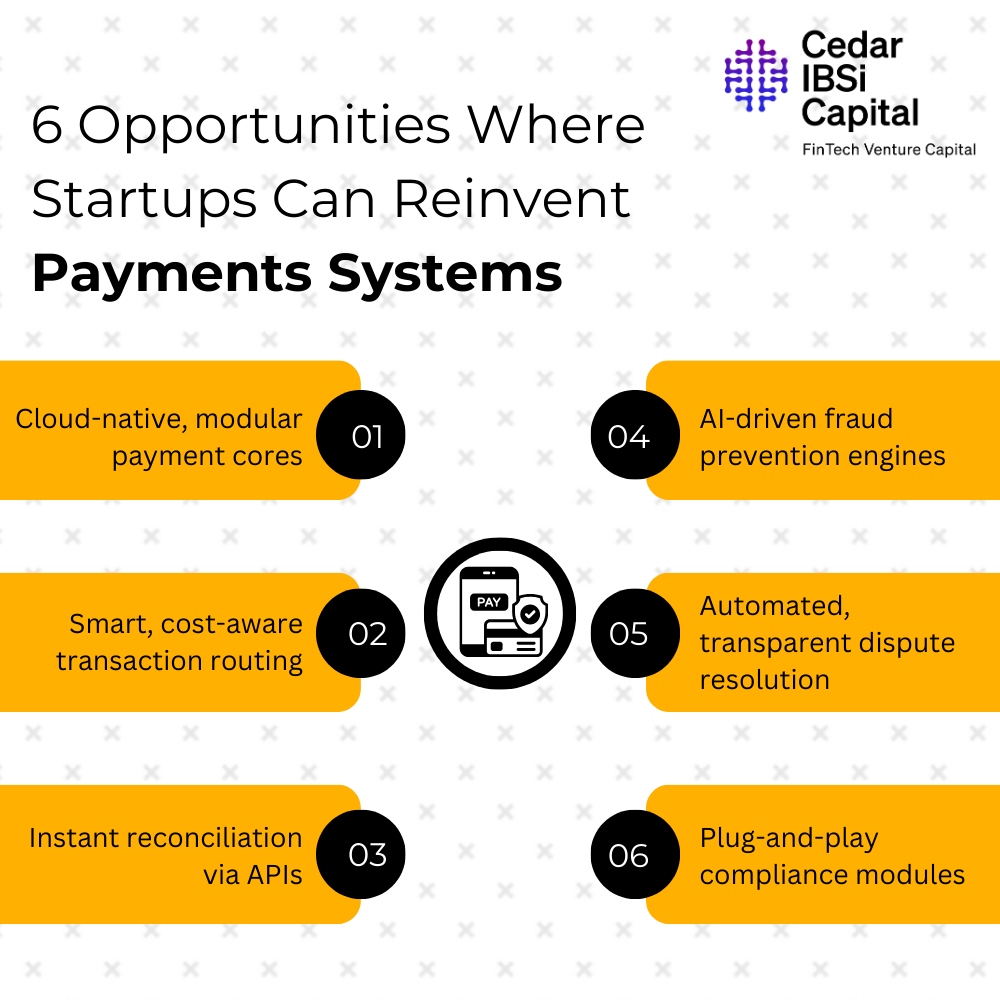

- Infrastructure Modernisation: Cloud-native, modular platforms replacing legacy cores

- Intelligent Routing: Cost-aware, issuer-aware, and risk-aware transaction switches

- Real-Time Reconciliation: APIs and dashboards for instant visibility

- Risk & Fraud Engines: ML-based scoring, behavioural analytics;

- Dispute Automation: Transparent workflows, customer self-service portals;

- Compliance-as-a-Service: Plug-and-play AML modules

Why Now?

- Regulatory tailwinds: Open banking, digital public infrastructure (like India’s DPI), and real-time payment mandates.

- Merchant demand: SMEs want faster onboarding, better visibility, and lower costs.

- Consumer expectations: Instant payments, zero friction, and secure experiences.

Final Thoughts

Legacy payment systems are not going away overnight—but they are ripe for disruption. Startups that understand the nuances of the payment stack and build for speed, transparency, and modularity will define the next decade of digital commerce.

The future of payments isn’t just about moving money—it’s about moving fast, smart, and with purpose.